http://benjaminstudebaker.com/2015/08/05/jeremy-corbyns-economic-plan-is-not-crazy/comment-page-1/#comment-214357

The following text is reproduced from "BENJAMIN STUDEBAKER".

Corbyn believes that the economy has not fully recovered and that economic demand is depressed:

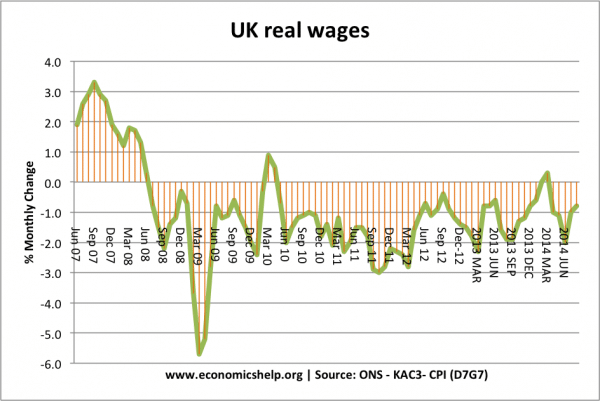

There’s a good argument that Britain is underperforming in the ways Corbyn highlights. British real wages have been falling consistently since the economic crisis:

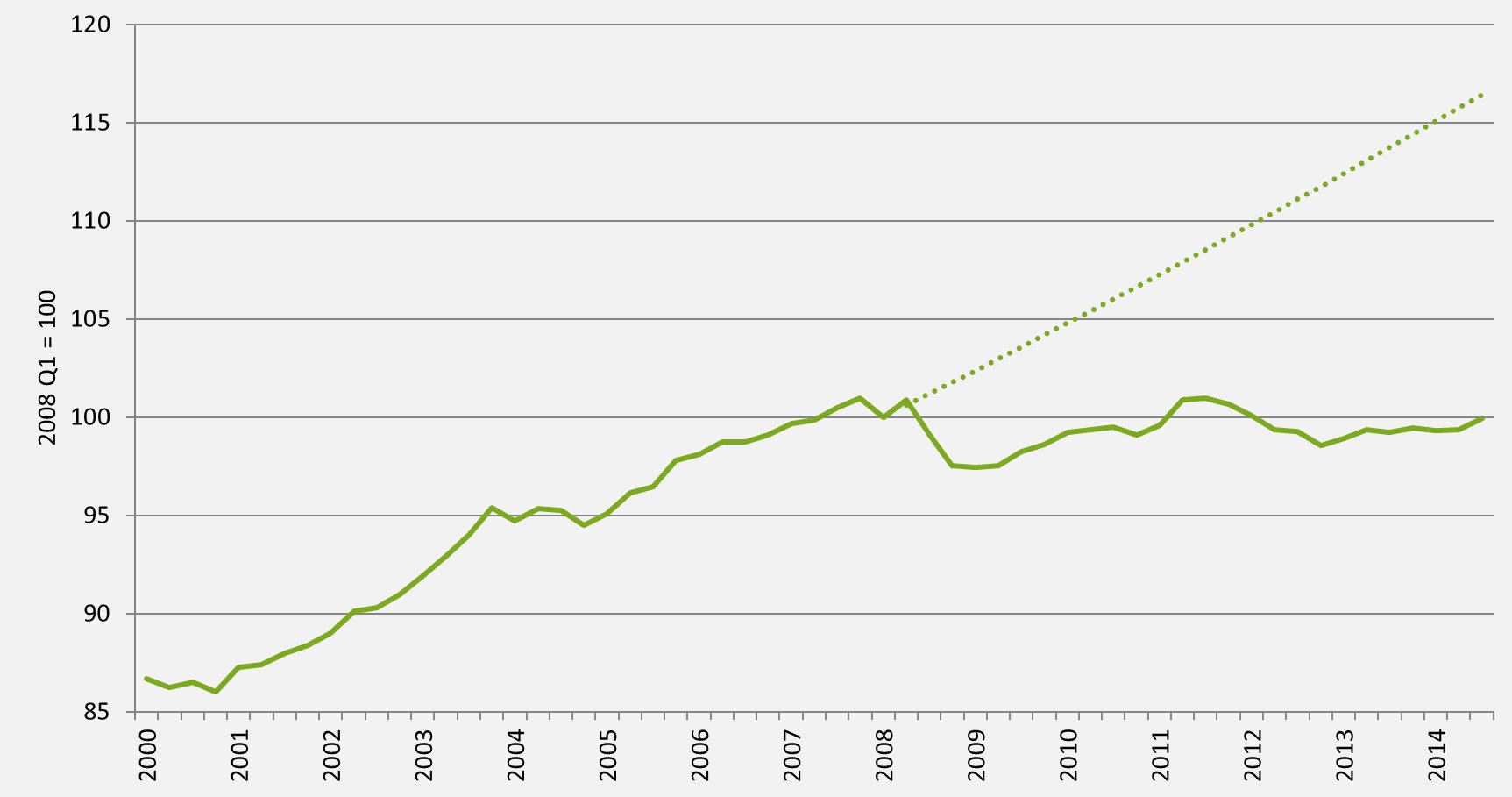

Productivity has not kept up with the historical trend line:

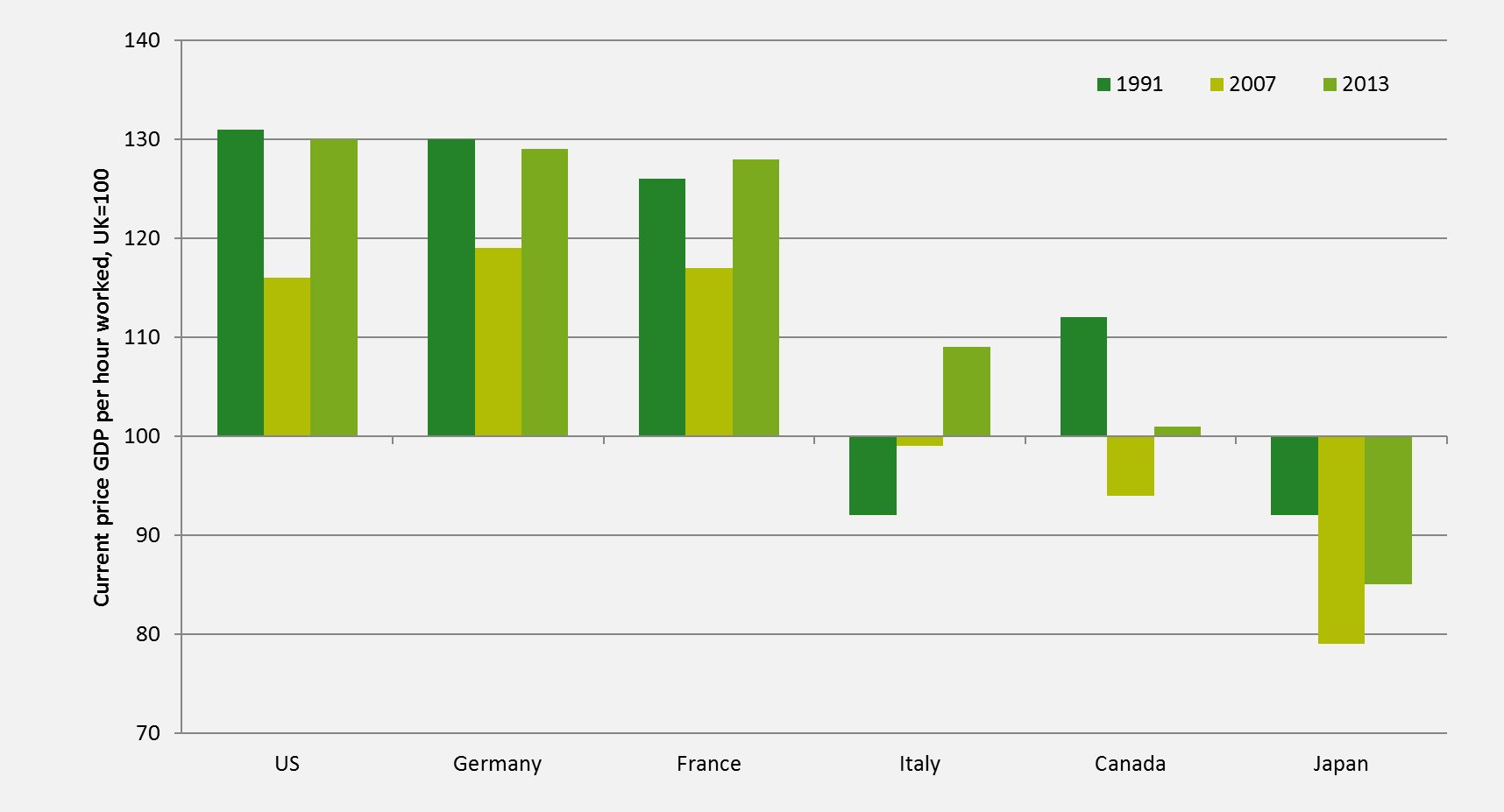

This is not an ailment that afflicts all countries equally–Britain has lost ground against all the other G7 countries since 2007 (UK = 100):

It is also true that in the last five years, the UK’s current account deficit has grown much larger:

Britain’s underemployment figures have been improving lately, but it still trails many European countries (many of which are stuck on the euro, which should seriously handicap them and give Britain an advantage):

So Corbyn’s criticisms of the UK economy under the Conservatives check out. To solve these problems, Corbyn wants the state to make some big investments in technology and infrastructure (energy, housing, transport, and digital). Ideally, these investments would create high skill, high wage jobs and improve Britain’s productivity and industrial competitiveness, allowing Britain to improve its current account and generate sustainable economic growth.

There is a good case for this–one of the advantages the state has over private investors is its ability to absorb large short-term losses in the interest of achieving far larger long-term gains. Investments that would bankrupt any private sector company are practical for the state because it has a lot more money to work with and a lot more access to credit. For these reasons, the state has long played a pivotal role in supporting major national projects, like the construction of the railroads or the grid. Many private sector innovations have their roots in technologies originally developed for military purposes by the state.

The question everyone wants answered is how Corbyn believes the UK can to pay for this. He proposes two strategies:

The Bank of England Strategy

The key thing that must be understood is that the Bank of England has already printed very large amounts of money and injected it into the economy. This was part of its quantitative easing (QE) strategy, which was also employed by the US Federal Reserve, the Bank of Japan, and, most recently, the European Central Bank. QE was first employed in the immediate aftermath of the global economic crisis. The goal of QE was to recapitalize the banks by taking governments bonds from the banks and exchanging them for newly printed currency. It was hoped that this would stabilize the financial sector and boost the wider economy by increasing the amount of money available for lending to the private sector.

At the time, the right was livid, warning that QE would lead to hyperinflation. In 2010, a number of business titans and economists wrote an open letter published in the Wall Street Journal warning the Federal Reserve of deadly consequences:

The UK hasn’t experienced high inflation either:

Indeed, in both countries, inflation is now dangerously close to zero. Deflation is very damaging to the economy–falling prices encourage people to wait to buy things, and this can rapidly bring the economy to a halt.

Why didn’t QE trigger significant inflation? QE sounds very inflationary–the state is literally printing money and handing it to banks–but if the economy is depressed, QE can maintain the level of economic activity necessary to prevent a recession without triggering a boom. QE was also criticized by the left because it gave the new money to bankers rather than consumers or the government. Because economic demand is depressed, banks and firms have little reason to spend the money they receive from the banks on expanding supply or on new projects. Instead, they invest the money in each other, inflating the stock market without creating enough job and productivity growth. Even as productivity and wages continue to lag, the FTSE 100 has performed very well over the past 5 years:

From where Corbyn is sitting, it appears that we’re printing money but failing to put it to use. So Corbyn wants to bypass the banks and directly fund his technology and infrastructure projects. Corbyn could do this with no significant adverse effects up until the point at which the economy really is running at capacity and inflation rises. In effect, his spending would be governed by the inflation rate rather than by the government budget. This is a radical, creative, and innovative government policy, and it would likely work. Britain’s current inflation rate is very close to 0%, so Corbyn could print and spend quite a bit of money through the Bank of England without seeing above-target inflation. Indeed, a little bit more inflation would be a good thing–most central banks try to run 2% inflation, and some economists recommend a high inflation target of at least 4%. So Corbyn would have lots of flexibility here.

The Soak the Rich Strategy

Alternatively, Corbyn also believes that he could find the money by closing tax loopholes and increasing enforcement of extant tax laws. Corbyn believes he could find £120 billion:

There is truth to this–Corbyn would certainly be taking significant amounts of money out of the hands of investors. Corbyn can defend the point by appealing to what I said before about how the FTSE is growing while productivity and wages stagnate. Corbyn can argue that the financial sector is not growing the real economy and that the money these investors have is idling. Corbyn can claim that by taking this money from them and having the state invest it in technology and infrastructure, Corbyn could generate more growth than the money presently generates idling in the stock market.

This is a direct challenge to the Conservative view that financialization is good for Britain and that more investment is always positive. Corbyn is implicitly alleging that the financial sector is not adequately distributing investment and that the state must step in to put the money to good use. This is very counter-intuitive to many people who have been taught to believe that the government is never more economically efficient than the private sector. This is why so many people are dismissing Corbyn’s plan as bonkers–they think it is impossible that Corbyn could increase growth by transferring money from rich private investors to the state because they think that rich private investors are the only true engine of growth. For this reason, they argue that any effort by Corbyn to collect the tax would result in a decrease in economic activity that would eliminate any revenue gains.

Who do you think is right? Thankfully, we don’t have to guess. Economists have already conducted significant research to determine the optimal tax rate for the rich, i.e. the rate that would raise the most real government revenue, taking into account the effects of taxation on work and investment. The research shows that the Conservatives dramatically underestimate the amount of tax that can be collected at gain–Diamond and Saez suggest that the top rate of tax could be 70% before the losses surpass the gains. They reviewed the literature on the Elasticity of Taxable Income and found a median value of 0.25 for the rich. This means that for every £1 increase in taxes, the rich will report £0.25 less income. That’s significant, but it’s much smaller than most people on the right believe, and it suggests that Corbyn really could find this money with the appropriate legislative toolkit. Add to this that there’s significant evidence that the specific things Corbyn wants to spend money on are really needed, and there’s a pretty good case for this policy.

There’s significant support in the literature for the claims Corbyn is making. The QE experience shows that Corbyn could definitely print and spend a significant amount of money on technology and infrastructure without pushing inflation above target. The research on optimal tax rates suggests that Corbyn will likely be able to find the tax revenue he’s looking for if the legislation he enacts is sufficiently robust. I am extremely confident that the Bank of England strategy would work and reasonably confident that the soak the rich strategy would as well. Corbyn should be taken seriously–those who oppose him must be made to engage with the optimal tax rate literature and they must be made to engage with what we’ve learned from the QE experience. The flippant dismissal we’re seeing of Corbyn and his ideas should not be allowed to pass unchecked.

The following text is reproduced from "BENJAMIN STUDEBAKER".

Jeremy Corbyn’s Economic Plan is Not Crazy

by Benjamin Studebaker

Over the past week, I’ve been hearing the rumors. They’re saying that Jeremy Corbyn is crazy–that he’s released an economic plan so radical, so incendiary, so madcap that no reasonable person could possibly support him for Labour leader. I thought to myself “Oh no Jeremy, what could you possibly have done to get these folks so riled up?” So I read the plan. It’s not crazy–indeed, there is significant support in the literature and in recent experience for what Corbyn is proposing. |

| Jeremy Corbyn: Educated at Adams' Grammar School in Newport, Shropshire |

Corbyn believes that the economy has not fully recovered and that economic demand is depressed:

To date, we have seen only the most feeble of upturns:He believes demand will still be depressed in 2020 and that there will be room for growth. He wants to unlock this untapped economic potential, improving the government’s fiscal position by increasing revenues and reducing demand for benefits by raising incomes.

• We have had the longest period of falling real wages since the 19th century

• A disastrous investment and productivity record

• A swelling balance of payments deficit

• The creation of army of low-paid, low skill, insecure, zero hours, bogus self-employment jobs. People are still worse off today than they were in 2008. The average household is still awaiting recovery.

There’s a good argument that Britain is underperforming in the ways Corbyn highlights. British real wages have been falling consistently since the economic crisis:

Productivity has not kept up with the historical trend line:

This is not an ailment that afflicts all countries equally–Britain has lost ground against all the other G7 countries since 2007 (UK = 100):

It is also true that in the last five years, the UK’s current account deficit has grown much larger:

Britain’s underemployment figures have been improving lately, but it still trails many European countries (many of which are stuck on the euro, which should seriously handicap them and give Britain an advantage):

So Corbyn’s criticisms of the UK economy under the Conservatives check out. To solve these problems, Corbyn wants the state to make some big investments in technology and infrastructure (energy, housing, transport, and digital). Ideally, these investments would create high skill, high wage jobs and improve Britain’s productivity and industrial competitiveness, allowing Britain to improve its current account and generate sustainable economic growth.

There is a good case for this–one of the advantages the state has over private investors is its ability to absorb large short-term losses in the interest of achieving far larger long-term gains. Investments that would bankrupt any private sector company are practical for the state because it has a lot more money to work with and a lot more access to credit. For these reasons, the state has long played a pivotal role in supporting major national projects, like the construction of the railroads or the grid. Many private sector innovations have their roots in technologies originally developed for military purposes by the state.

The question everyone wants answered is how Corbyn believes the UK can to pay for this. He proposes two strategies:

- The Bank of England Strategy: replace quantitative easing with an equivalent program that invests new money directly into technology and infrastructure, bypassing the banks.

- The Soak the Rich Strategy: eliminate tax loopholes and tax subsidies for the wealthy and corporations and use the money raised to create a National Investment Bank, similar to the sovereign wealth funds that countries like Norway have.

The Bank of England Strategy

The key thing that must be understood is that the Bank of England has already printed very large amounts of money and injected it into the economy. This was part of its quantitative easing (QE) strategy, which was also employed by the US Federal Reserve, the Bank of Japan, and, most recently, the European Central Bank. QE was first employed in the immediate aftermath of the global economic crisis. The goal of QE was to recapitalize the banks by taking governments bonds from the banks and exchanging them for newly printed currency. It was hoped that this would stabilize the financial sector and boost the wider economy by increasing the amount of money available for lending to the private sector.

At the time, the right was livid, warning that QE would lead to hyperinflation. In 2010, a number of business titans and economists wrote an open letter published in the Wall Street Journal warning the Federal Reserve of deadly consequences:

We believe the Federal Reserve’s large-scale asset purchase plan (so-called “quantitative easing”) should be reconsidered and discontinued. We do not believe such a plan is necessary or advisable under current circumstances. The planned asset purchases risk currency debasement and inflation, and we do not think they will achieve the Fed’s objective of promoting employment.What happened? The warnings proved unfounded–inflation did not skyrocket in the US:

The UK hasn’t experienced high inflation either:

Indeed, in both countries, inflation is now dangerously close to zero. Deflation is very damaging to the economy–falling prices encourage people to wait to buy things, and this can rapidly bring the economy to a halt.

Why didn’t QE trigger significant inflation? QE sounds very inflationary–the state is literally printing money and handing it to banks–but if the economy is depressed, QE can maintain the level of economic activity necessary to prevent a recession without triggering a boom. QE was also criticized by the left because it gave the new money to bankers rather than consumers or the government. Because economic demand is depressed, banks and firms have little reason to spend the money they receive from the banks on expanding supply or on new projects. Instead, they invest the money in each other, inflating the stock market without creating enough job and productivity growth. Even as productivity and wages continue to lag, the FTSE 100 has performed very well over the past 5 years:

From where Corbyn is sitting, it appears that we’re printing money but failing to put it to use. So Corbyn wants to bypass the banks and directly fund his technology and infrastructure projects. Corbyn could do this with no significant adverse effects up until the point at which the economy really is running at capacity and inflation rises. In effect, his spending would be governed by the inflation rate rather than by the government budget. This is a radical, creative, and innovative government policy, and it would likely work. Britain’s current inflation rate is very close to 0%, so Corbyn could print and spend quite a bit of money through the Bank of England without seeing above-target inflation. Indeed, a little bit more inflation would be a good thing–most central banks try to run 2% inflation, and some economists recommend a high inflation target of at least 4%. So Corbyn would have lots of flexibility here.

The Soak the Rich Strategy

Alternatively, Corbyn also believes that he could find the money by closing tax loopholes and increasing enforcement of extant tax laws. Corbyn believes he could find £120 billion:

The £120bn figure is made up from:The right argues that even if this money theoretically might be collectible on paper, the act of trying to collect it will cause it to vanish. This is because the right believes that there is no substantive difference between reducing tax debt, avoidance, and evasion and tax increases–both of these policies take more money from taxpayers, albeit by different legal means. The right believes that tax increases will cause brain drain, as innovators and investors flee the UK’s high rates. They also believe that increases will discourage private sector investment. Since enforcement and rate increases both collect more tax, the right believes both policies will have the same results.

• about £20bn in tax debt, uncollected by HMRC which continues to suffer budget and staffing cuts (only partially reversed in the last Budget)

• another £20bn in tax avoidance

• and a further £80bn in tax evasion.

There is truth to this–Corbyn would certainly be taking significant amounts of money out of the hands of investors. Corbyn can defend the point by appealing to what I said before about how the FTSE is growing while productivity and wages stagnate. Corbyn can argue that the financial sector is not growing the real economy and that the money these investors have is idling. Corbyn can claim that by taking this money from them and having the state invest it in technology and infrastructure, Corbyn could generate more growth than the money presently generates idling in the stock market.

This is a direct challenge to the Conservative view that financialization is good for Britain and that more investment is always positive. Corbyn is implicitly alleging that the financial sector is not adequately distributing investment and that the state must step in to put the money to good use. This is very counter-intuitive to many people who have been taught to believe that the government is never more economically efficient than the private sector. This is why so many people are dismissing Corbyn’s plan as bonkers–they think it is impossible that Corbyn could increase growth by transferring money from rich private investors to the state because they think that rich private investors are the only true engine of growth. For this reason, they argue that any effort by Corbyn to collect the tax would result in a decrease in economic activity that would eliminate any revenue gains.

Who do you think is right? Thankfully, we don’t have to guess. Economists have already conducted significant research to determine the optimal tax rate for the rich, i.e. the rate that would raise the most real government revenue, taking into account the effects of taxation on work and investment. The research shows that the Conservatives dramatically underestimate the amount of tax that can be collected at gain–Diamond and Saez suggest that the top rate of tax could be 70% before the losses surpass the gains. They reviewed the literature on the Elasticity of Taxable Income and found a median value of 0.25 for the rich. This means that for every £1 increase in taxes, the rich will report £0.25 less income. That’s significant, but it’s much smaller than most people on the right believe, and it suggests that Corbyn really could find this money with the appropriate legislative toolkit. Add to this that there’s significant evidence that the specific things Corbyn wants to spend money on are really needed, and there’s a pretty good case for this policy.

There’s significant support in the literature for the claims Corbyn is making. The QE experience shows that Corbyn could definitely print and spend a significant amount of money on technology and infrastructure without pushing inflation above target. The research on optimal tax rates suggests that Corbyn will likely be able to find the tax revenue he’s looking for if the legislation he enacts is sufficiently robust. I am extremely confident that the Bank of England strategy would work and reasonably confident that the soak the rich strategy would as well. Corbyn should be taken seriously–those who oppose him must be made to engage with the optimal tax rate literature and they must be made to engage with what we’ve learned from the QE experience. The flippant dismissal we’re seeing of Corbyn and his ideas should not be allowed to pass unchecked.

Comments

Post a Comment